Roth 401(k)

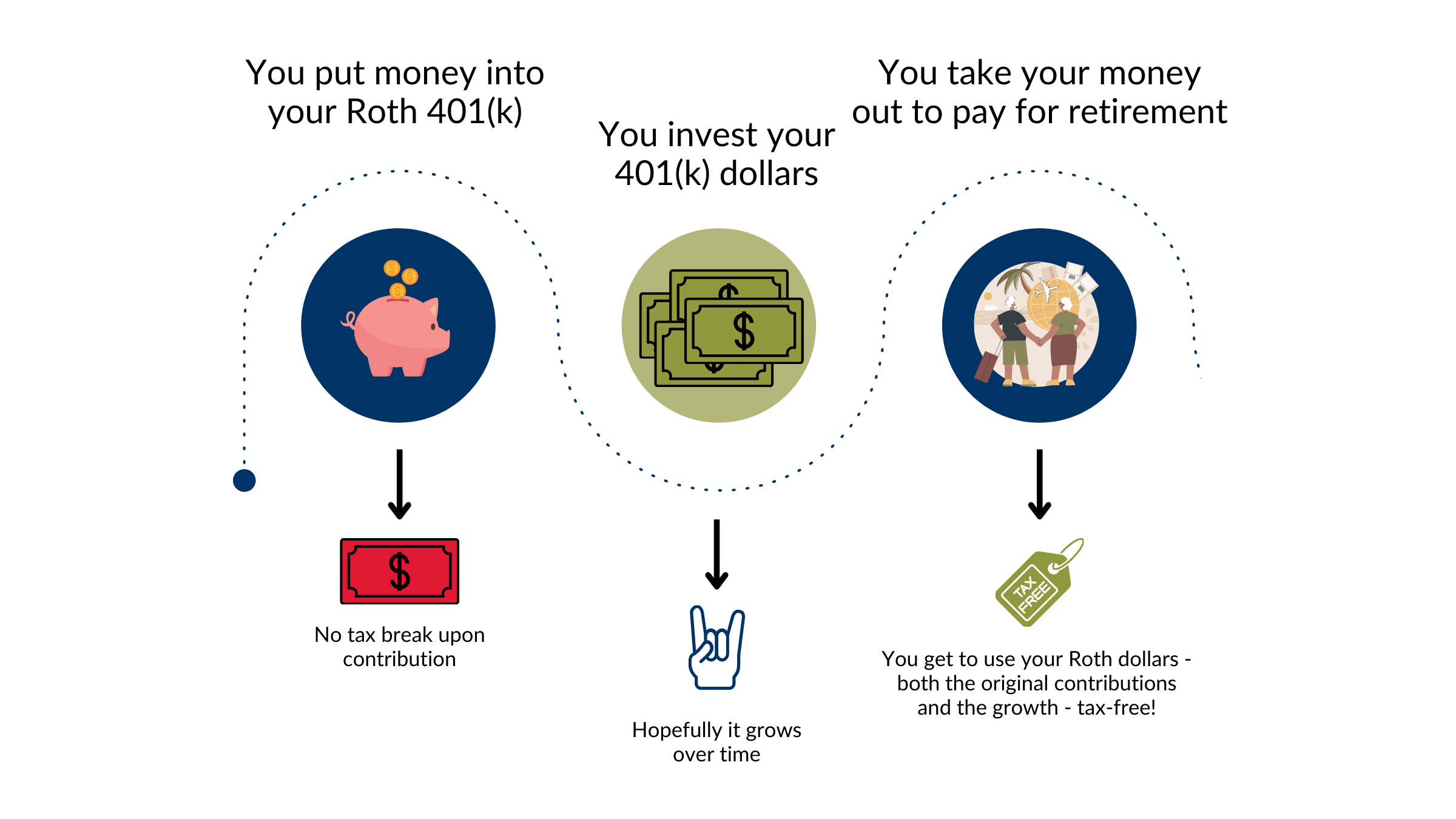

A Roth 401(k) is a retirement savings approach where you put in money that you've already paid taxes on, or put another way, you do not get a tax break when you put the money in. Despite not getting a tax break when you contribute, the good news is that the money grows tax-free. When you take it out in retirement, assuming you’ve met some thresholds, you won't have to pay any taxes on it, not even on the earnings. It can be great for people who want to reward their future self. So, you pay taxes now and enjoy tax-free money later!

This retirement savings approach can be used in Next Best Step 4 and/or in Next Best Step 8.

Using a Roth 401(k) would most commonly be applicable in steps:

How to elect the after-tax 401(k)

If you decide that the Roth 401(k) is right for you, then you can either login to NetBenefits.com or go to the NetBenefits app. From there, navigate to the Contributions section. The after-tax section will be labeled Roth.

Roth 401(k) Example

Meet John, a 35 year old Delta employee:

He is making $50,000 a year.

He decides to save 6% on a Roth basis in the 401(k).

John still receives the 6% match and the 3% automatic contribution, making his total contribution 15%.

Even though his own contributions are going into the Roth 401(k), both the 6% match and the automatic 3% contributions go into the pretax 401(k).

The 6% that John saved in the Roth 401(k) is $3,000 and the 9% (6% match + 3% automatic) Delta contribution is $4,500. Because John chose to save his 6% in the Roth 401(k) he pays taxes on the entirety of the $50,000 of his income, including the $3,000 that he put into the Roth 401(k) (ignoring all other deductions, credits, exemptions, etc.). If John had chosen to contribute his 6% on a pre-tax basis, he would pay taxes on $47,000 of income.

Let’s say that after 20 years his contributions from this year have doubled twice [placeholder - let’s create a library item for the rule of 72], making his Roth contributions worth $12,000 ($3,000 X 2 X 2) and his Delta contributions worth $18,000 ($4,500 X 2 X 2).

John withdraws the entirety of these amounts.

The $12,000 of his Roth balance can be taken out completely tax-free.

The $18,000 of his pretax balance is subject to taxes. Let’s hypothetically say that his tax rate is 12% Federal and 5% state. The amount of the $18,000 that he would actually receive would be $14,940 ($18,000 X 0.83).

This outcome doesn’t make Roth better than pretax, per se, but it does show that saving in Roth rewards John’s future self by paying the taxes upfront.

Why would someone choose Roth 401(k)?

This approach is often-times, though not always, used:

By people early in their careers: Because dollars go into the account after paying taxes, the generally accepted truth is that Roth is better when a person’s income is lower now than it would be anticipated to be in the future.

By people who are believe tax rates in general will be higher in the future: Think Congress is going to, or perhaps will have to, increase taxes in the future. Saving in Roth allows you to shelter the gains from future taxation.

By people who want to diversify the way they are saving: Because employer contributions by default go into the pre-tax category, by saving in the Roth 401(k), savers are in effect diversifying the future tax situation. Diversification provides an insurance of sorts against future tax law or income level changes.

FAQs

-

There are no income limitations to utilizing the Roth 401(k). This is commonly misunderstood as there are income limitations to the Roth IRA, but keep in mind that the Roth 401(k) and the Roth IRA are different account types.

-

You do not have to save in just one of the two options. If you're looking to meet the match you can do any combination of pretax and/or Roth

6% pretax

6% Roth

1% pretax/5% Roth

3% pretax/3% Roth

So on.

-

Yes. As long as you are saving 6% in the 401(k), regardless of savings type, you'll receive the match.